+852 2830 9999

+852 2830 9999

+852 6699 6196

+852 6699 6196

Wingate has been providing high quality one-stop services since the Year 2000.

Wingate's Professional Services

中環廣場

Wanchai Central Plaza

![]() Room 3208, 32/F, Central Plaza, 18 Harbour Road, Wanchai (MTR Exit A5)

Room 3208, 32/F, Central Plaza, 18 Harbour Road, Wanchai (MTR Exit A5)

View more>>

News

2023-24 Budget - New Highlights

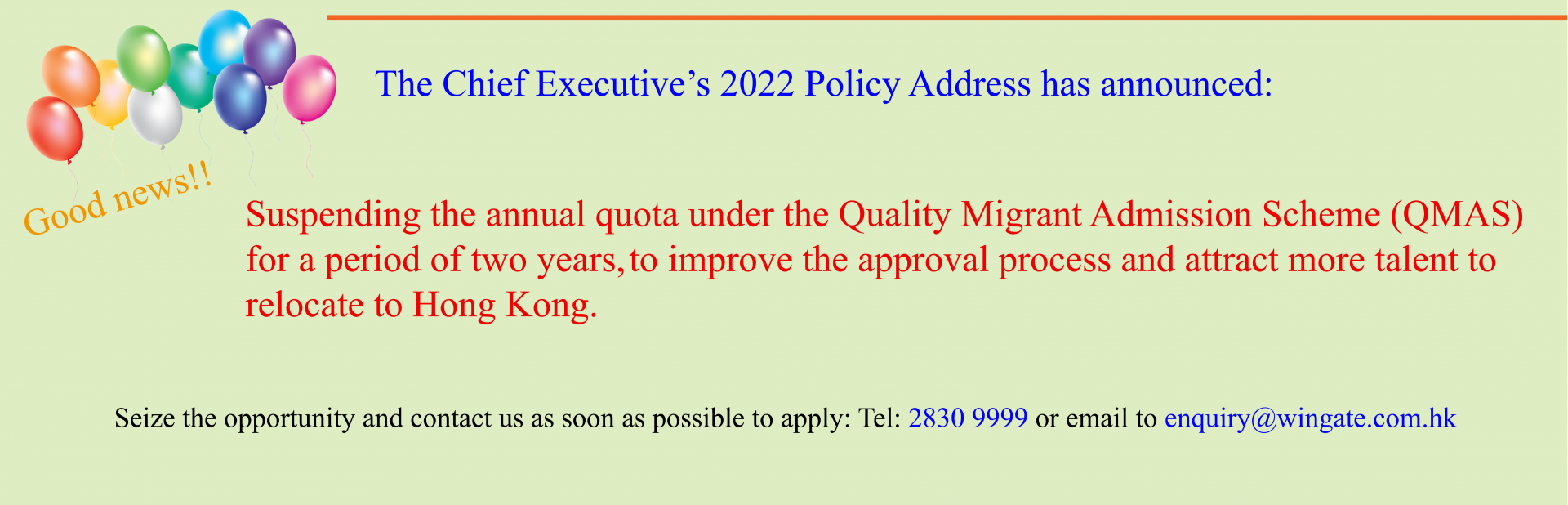

Capital Investment Entrant Scheme (CIES) :

applicants shall make investment at a certain amount in...

")

New Individual Office Room Special Offer (Tokyo, Japan)

We can help you set up an office in Tokyo, Japan stress free with our fully furnished, brand new off...

Business registration fees no longer waived in Budget 2023

Latest news!

The 2023 Budget will no longer waive the business registration fee (HKD2,000). If you ...

Wingate’s License Members and Awards

- Wingate Business Limited

Trust or Company Service Provider License (License No.: TC001745) - Wingate Professional Secretary Limited

Trust or Company Service Provider License (License No.: TC000299) - HSBC

Business Advisor Award

Current HK Time:

Office Hours: Monday - Friday: 9:00am – 6:00pm

Address: Room 3208, 32/F, Central Plaza, 18 Harbour Road, Wanchai (MTR Exit A5)

Tel : +852 2830 9999

Fax: +852 2830 9998

Email: enquiry@wingate.com.hk